Debt Consolidation 2026: Reduce Payments 25% with New Loans

Anúncios

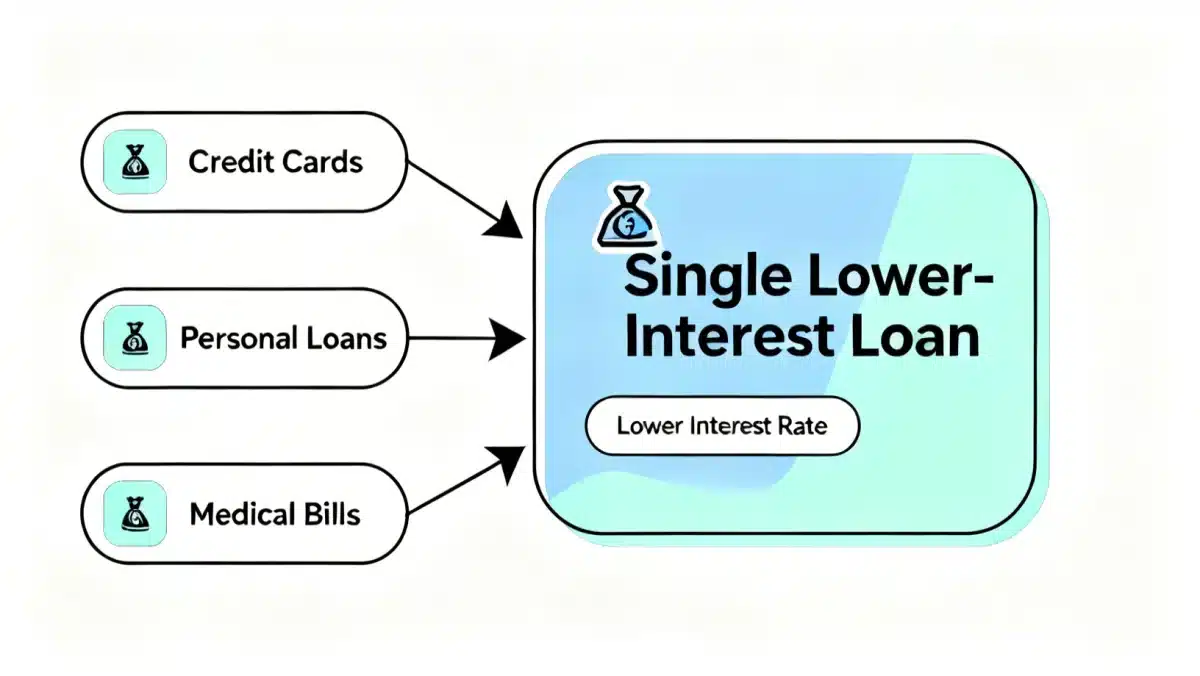

Debt consolidation in 2026 offers a strategic path to financial relief, allowing individuals to streamline multiple debts into a single, potentially lower-interest loan, aiming for a significant reduction in monthly payments.

Are you feeling overwhelmed by multiple debts and looking for a way to simplify your finances? Debt consolidation in 2026: Reducing Your Monthly Payments by 25% with New Loan Options could be the strategic move you need to regain control. This approach can significantly ease your financial burden, offering a clearer path to debt freedom.

Anúncios

Understanding debt consolidation in 2026

Debt consolidation involves combining several smaller debts into a single, larger loan, ideally with a lower interest rate or more favorable terms. This strategy is not new, but the financial landscape of 2026 presents unique opportunities and considerations. As interest rates fluctuate and new financial products emerge, understanding the contemporary options is crucial for maximizing benefits.

Anúncios

The primary goal of consolidating debt is often to simplify payments and reduce the overall cost of borrowing. Instead of managing multiple due dates and varying interest rates, you have one payment to track. This can lead to less stress and a clearer picture of your financial obligations, making it easier to budget and adhere to a repayment plan.

The evolving financial landscape

The year 2026 sees a continued evolution in lending practices, driven by technological advancements and shifts in economic policies. Digital lenders are offering more personalized loan products, and traditional banks are adapting to stay competitive. This means consumers have a wider array of choices, but also a greater need for due diligence in selecting the right option.

- Technological integration: AI-driven algorithms are now common in loan underwriting, potentially offering quicker approvals and more tailored rates based on individual credit profiles.

- Increased competition: A crowded market of lenders, from fintech startups to established institutions, often translates to better rates and terms for consumers.

- Regulatory changes: New consumer protection laws and lending regulations might influence eligibility criteria and loan product offerings, making it essential to stay informed.

Ultimately, debt consolidation in 2026 is about leveraging these new opportunities to secure a financial arrangement that genuinely improves your fiscal health. It requires careful planning and a thorough understanding of your current financial standing and future goals.

Benefits of consolidating your debt

The advantages of consolidating debt extend beyond mere simplification. For many, it represents a significant step towards financial stability and peace of mind. One of the most compelling benefits is the potential to reduce your monthly payments, sometimes by as much as 25% or more, depending on your current debt structure and the terms of your new loan.

Imagine freeing up a considerable portion of your monthly income that was previously allocated to high-interest debt. This extra cash flow can be used for savings, investments, or simply to alleviate daily financial pressure. It can also help you avoid falling further into debt by giving you more breathing room in your budget.

Streamlined financial management

Having one monthly payment instead of several is a game-changer for many. It reduces the likelihood of missing payments, which can negatively impact your credit score and incur late fees. A single payment also makes budgeting much simpler, as you have a clear, consistent expense to factor into your financial plan.

- Reduced interest rates: Often, a consolidation loan comes with a lower overall interest rate than the combined rates of your individual debts, saving you money over the long term.

- Improved credit score potential: Consistently making on-time payments on a single loan can positively impact your credit score over time, as payment history is a significant factor.

- Fixed repayment schedule: Many consolidation loans offer a fixed repayment period, providing a clear end date for your debt and motivating you to stick to the plan.

However, it’s important to remember that while consolidation can reduce your monthly payments, it doesn’t eliminate the debt itself. It merely reorganizes it. The discipline to avoid accumulating new debt after consolidating is crucial for long-term success.

New loan options in 2026 for debt consolidation

The lending landscape in 2026 offers diverse options for debt consolidation, catering to various financial situations and credit profiles. Beyond traditional personal loans, new products and platforms are emerging that provide more flexibility and potentially better rates. Understanding these options is key to selecting the most suitable path for your financial goals.

Personal loans remain a popular choice, often unsecured, meaning they don’t require collateral. These loans typically have fixed interest rates and repayment terms, offering predictability. However, eligibility and interest rates are heavily dependent on your credit score and income.

Exploring innovative lending solutions

Beyond standard personal loans, 2026 brings forward several innovative avenues for debt consolidation. These options often leverage technology to provide more accessible or tailored solutions, particularly for those with less-than-perfect credit or unique financial circumstances.

- Peer-to-peer lending platforms: These platforms connect borrowers directly with individual investors, sometimes resulting in more flexible terms and competitive rates compared to traditional banks.

- Balance transfer credit cards (with extended 0% APR): While not a loan, some credit cards in 2026 offer significantly longer 0% introductory APR periods, allowing you to pay down high-interest debt without incurring interest for a substantial time. Careful management is essential to pay off the balance before the promotional period ends.

- Secured personal loans: For those with significant assets, secured loans (using collateral like a car or savings account) can offer lower interest rates due to reduced risk for the lender.

- Home equity loans or lines of credit (HELOCs): If you own a home, leveraging your home equity can provide access to larger loan amounts at lower interest rates. However, this option carries the risk of losing your home if you default.

Each of these options has its own set of pros and cons, and the best choice depends on your individual financial health, risk tolerance, and the amount of debt you need to consolidate. Thorough research and potentially consulting with a financial advisor are highly recommended.

Qualifying for a debt consolidation loan in 2026

Securing a debt consolidation loan in 2026 involves meeting specific eligibility criteria set by lenders. While requirements can vary, understanding the general expectations will help you prepare and increase your chances of approval. Lenders primarily assess your creditworthiness, income stability, and debt-to-income ratio.

Your credit score is often the most critical factor. A higher credit score signals to lenders that you are a responsible borrower, making you eligible for better interest rates and terms. If your credit score isn’t ideal, there are still options, but they might come with higher interest rates.

Key eligibility factors

Lenders evaluate several aspects of your financial profile to determine your eligibility and the terms of your loan. Being prepared with accurate information about these factors can expedite the application process.

- Credit score: Aim for a good to excellent credit score (typically 670 and above) to qualify for the most favorable rates. If your score is lower, focus on improving it before applying or explore options specifically designed for fair or poor credit.

- Income and employment history: Lenders want to see stable income and employment to ensure you can make regular payments. They will often request pay stubs, tax returns, or bank statements.

- Debt-to-income (DTI) ratio: This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to cover new loan payments.

- Collateral (for secured loans): If you opt for a secured loan, the value and type of collateral you offer will be assessed.

It’s advisable to check your credit report and score well before applying for a loan. This allows you to identify and dispute any errors and understand where you stand. Some lenders also offer pre-qualification, which can give you an idea of potential rates without impacting your credit score.

Strategies for reducing monthly payments by 25%

Achieving a 25% reduction in monthly payments through debt consolidation is an ambitious yet attainable goal. It requires a strategic approach that combines securing the right loan with careful financial planning. The key lies in finding a loan with a significantly lower interest rate or a longer repayment term, or ideally, both.

Start by meticulously calculating your current total monthly debt payments and the average interest rate you’re paying across all your debts. This baseline will help you determine how much of a reduction you need and whether a consolidation loan can realistically achieve it.

Optimizing your consolidation strategy

Several strategies can help you maximize your savings and reach that 25% reduction target. It’s not just about getting a new loan; it’s about making that loan work effectively for your financial situation.

- Shop around for the best rates: Don’t settle for the first offer. Compare interest rates, fees, and terms from multiple lenders, including traditional banks, credit unions, and online lenders. Utilize online comparison tools to streamline this process.

- Improve your credit score: Even a slight improvement in your credit score can lead to a better interest rate, which directly impacts your monthly payment. Pay down small debts, resolve any credit report errors, and make all payments on time.

- Consider a longer repayment term: While a longer term means paying more interest over the life of the loan, it can significantly lower your monthly payments. Balance this against your goal of becoming debt-free.

- Negotiate with lenders: In some cases, lenders may be willing to negotiate interest rates or terms, especially if you have a strong credit history or a compelling reason for consolidation.

Remember that reducing your monthly payments by 25% will require careful calculation and a commitment to your new repayment plan. Avoid the temptation to take on new debt once you’ve consolidated, as this can undo all your efforts.

Potential pitfalls and how to avoid them

While debt consolidation offers significant benefits, it’s not without its risks. Understanding these potential pitfalls and taking proactive steps to avoid them is crucial for a successful consolidation strategy. A common mistake is using the freed-up credit to accumulate new debt, leading to a worse financial position than before.

Another pitfall is focusing solely on the lowest monthly payment without considering the total cost of the loan over its lifetime. A longer repayment term might offer a lower monthly payment but could result in paying more in interest overall.

Navigating common challenges

Being aware of potential issues and having a plan to mitigate them can safeguard your financial well-being after consolidating your debt. It’s about making informed decisions and maintaining financial discipline.

- Accumulating new debt: The most significant risk is falling back into debt. Once consolidated, close old credit lines or cut up credit cards to remove temptation. Focus on building an emergency fund to avoid relying on credit for unexpected expenses.

- Higher overall cost: A longer repayment period, while reducing monthly payments, can sometimes lead to a higher total interest paid. Calculate the total cost of the consolidation loan versus your current debts to ensure you’re truly saving money.

- Impact on credit score: While consolidation can eventually help your credit, initially, applying for a new loan can cause a temporary dip due to a hard inquiry. Also, closing old accounts can slightly reduce your available credit and impact your credit utilization ratio.

- Hidden fees: Some consolidation loans come with origination fees, balance transfer fees, or prepayment penalties. Read the fine print carefully to understand all associated costs.

To avoid these pitfalls, create a strict budget, commit to your new repayment plan, and seek professional financial advice if you’re unsure about the best course of action. Discipline is your greatest asset in making debt consolidation a success.

Future outlook: debt consolidation beyond 2026

The landscape of debt consolidation is continuously evolving, and while we focus on 2026, it’s beneficial to consider what the future holds. Trends suggest even greater personalization of financial products, increased use of AI in risk assessment, and a stronger emphasis on financial literacy and wellness programs from lenders. These developments could make debt consolidation even more accessible and effective in the coming years.

As economic conditions shift, so too will the strategies for managing debt. Staying informed about these changes will be key to making the most advantageous financial decisions for your future.

Emerging trends and long-term planning

Looking ahead, several trends are poised to shape the future of debt consolidation, offering both new opportunities and challenges for consumers seeking financial relief.

- Hyper-personalized lending: Expect AI and machine learning to offer even more customized loan products based on granular financial data, potentially leading to fairer rates for a wider range of borrowers.

- Blockchain and decentralized finance (DeFi): While still nascent, DeFi platforms could eventually offer alternative lending solutions with lower overheads, potentially disrupting traditional banking models.

- Financial wellness programs: Lenders may increasingly integrate financial education and counseling into their offerings, helping borrowers not just consolidate debt but also prevent future financial distress.

- Environmental, Social, and Governance (ESG) considerations: As consumer awareness grows, some lenders might offer consolidation loans with favorable terms to borrowers who demonstrate commitment to sustainable financial practices.

For individuals, this means a future where proactive financial management becomes even more critical. Regularly reviewing your financial health, understanding emerging loan options, and continuously improving your creditworthiness will be essential for navigating the debt landscape effectively long after 2026. The goal remains the same: achieving lasting financial stability and freedom.

| Key Aspect | Brief Description |

|---|---|

| Goal | Combine debts into one loan, reduce monthly payments by 25%. |

| New Loan Options | Personal loans, P2P lending, balance transfer cards, home equity loans. |

| Eligibility | Credit score, income stability, debt-to-income ratio are key factors. |

| Avoid Pitfalls | Don’t accrue new debt; compare total costs, not just monthly payments. |

Frequently asked questions about debt consolidation in 2026

Debt consolidation combines multiple debts, like credit card balances or personal loans, into a single new loan. This new loan typically has a lower interest rate and a single monthly payment, simplifying your finances and potentially reducing your total monthly outflow.

Yes, achieving a 25% reduction is possible, especially if you secure a consolidation loan with a significantly lower interest rate or a longer repayment term than your current debts. Success depends on your credit profile and the terms you qualify for.

In 2026, options include traditional personal loans, peer-to-peer lending, balance transfer credit cards with extended 0% APR periods, and secured loans like home equity options. Evaluate each based on your financial situation.

The primary risks include accumulating new debt after consolidation, potentially paying more in total interest over a longer loan term, and initial temporary dips in your credit score from new credit inquiries. Discipline is key to avoiding these.

Focus on improving your credit score by making timely payments and reducing existing debt. Additionally, ensure you have stable income and a manageable debt-to-income ratio. Shopping around and comparing offers from multiple lenders is also crucial.

Conclusion

Navigating the complexities of personal finance can be challenging, but debt consolidation in 2026: Reducing Your Monthly Payments by 25% with New Loan Options stands out as a powerful tool for those seeking financial reprieve. By carefully assessing your current debt, exploring the diverse loan products available, and committing to responsible financial habits, you can significantly lighten your monthly burden and pave the way for a more secure financial future. This strategic approach, when executed thoughtfully, offers not just a temporary fix, but a viable pathway to lasting financial stability.