Student Loan Forgiveness Programs 2026: New Pathways to Debt Relief

Anúncios

Student loan forgiveness programs in 2026 are set to introduce new pathways to debt relief and expand eligibility, offering crucial financial assistance to a broader range of borrowers across the United States.

Are you navigating the complex landscape of student loan debt and wondering what the future holds? As we look towards 2026, significant changes and new opportunities are emerging within student loan forgiveness programs 2026: new pathways to debt relief and eligibility that could profoundly impact your financial future. Understanding these updates is crucial for anyone seeking to alleviate the burden of educational debt.

Anúncios

understanding the evolving landscape of student loan forgiveness

The arena of student loan forgiveness is constantly shifting, influenced by legislative changes, economic factors, and policy adjustments. For 2026, borrowers can anticipate a more refined and potentially more accessible framework for debt relief. These changes are often designed to address long-standing issues within the student loan system, aiming to provide more equitable and sustainable solutions for millions of Americans burdened by educational debt.

Anúncios

Many past programs faced criticism for their complexity and limited reach. The focus for 2026 appears to be on streamlining processes, clarifying eligibility, and expanding the scope of who can benefit. This includes not only federal loan programs but also potential new initiatives that might address specific demographics or economic hardships. Staying informed about these evolving policies is the first step toward securing your financial well-being.

key policy shifts and their impact

Recent legislative discussions and proposed policies suggest a move towards more inclusive forgiveness options. These shifts could mean a simplification of application processes and a broader interpretation of what constitutes ‘public service’ or ‘financial hardship.’ Understanding these nuances will be essential for borrowers preparing to apply for relief in the coming years.

- Expanded eligibility criteria: More borrowers may qualify for existing programs.

- Simplified application processes: Reducing administrative hurdles for applicants.

- Focus on economic hardship: New considerations for individuals facing financial difficulties.

These policy shifts are not merely incremental; they represent a concerted effort to recalibrate the balance between educational access and financial responsibility. The goal is to ensure that higher education remains a viable path for all, without leading to insurmountable debt. Borrowers should closely monitor official government announcements and financial aid resources for the most accurate and up-to-date information regarding these changes.

navigating public service loan forgiveness (pslf) in 2026

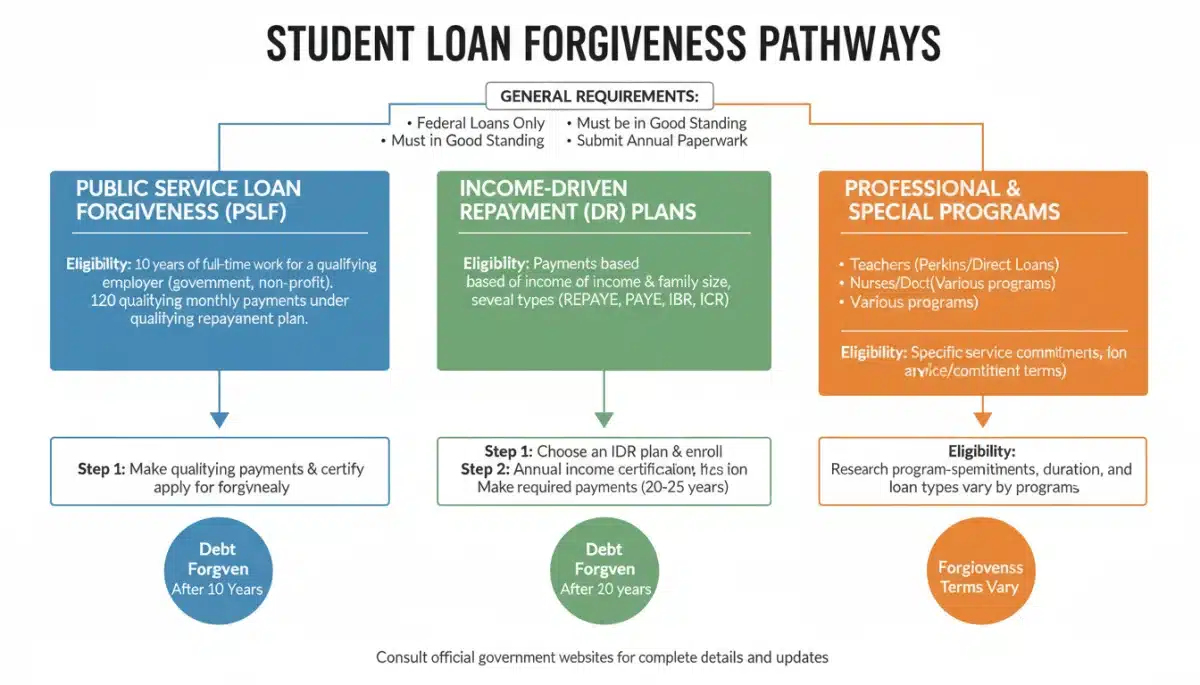

Public Service Loan Forgiveness (PSLF) remains a cornerstone of federal debt relief, offering complete forgiveness for direct loans after 120 qualifying payments made while working full-time for a qualifying employer. For 2026, the program is expected to continue its trajectory of reform, building on temporary waivers that have already simplified eligibility and expanded access. These ongoing improvements aim to make PSLF more predictable and less administratively burdensome for dedicated public servants.

The core tenets of PSLF — working in government, non-profit organizations, or other qualifying public service roles — will likely remain. However, the definition of what constitutes a ‘qualifying payment’ or ‘full-time employment’ might see further clarification or expansion. Borrowers currently on track for PSLF, or those considering a career in public service, should pay close attention to any updated guidance from the Department of Education.

understanding qualifying employment and payments

Qualifying employment for PSLF generally includes federal, state, local, or tribal government organizations, as well as not-for-profit organizations that are tax-exempt under Section 501(c)(3) of the Internal Revenue Code. Certain other non-profit organizations that provide specific public services may also qualify. The key is to ensure your employer meets these criteria and that you are working full-time for them.

- Employer certification: Regularly certify your employment to track progress accurately.

- Eligible loan types: Only federal direct loans qualify; consolidate other federal loans if necessary.

- Payment plans: Must be on an income-driven repayment (IDR) plan for qualifying payments.

The temporary PSLF waivers introduced in previous years have allowed many borrowers to count payments that previously didn’t qualify, bringing them closer to forgiveness. While these specific waivers may not extend indefinitely into 2026, the lessons learned from their implementation are likely to inform permanent program changes, making PSLF a more robust and reliable pathway to debt relief for those serving their communities.

income-driven repayment (idr) plans and their role in 2026

Income-Driven Repayment (IDR) plans are a vital component of student loan management, especially for those seeking eventual forgiveness. These plans adjust monthly payments based on a borrower’s income and family size, with any remaining balance forgiven after 20 or 25 years of payments. For 2026, new IDR options, or modifications to existing ones, are anticipated to make these plans even more accessible and beneficial.

The Biden-Harris administration has already introduced the SAVE plan, which significantly reduces monthly payments for many borrowers and offers faster forgiveness for those with smaller loan balances. This trend towards more generous IDR plans is expected to continue, potentially including further reductions in discretionary income calculations or shorter forgiveness timelines for certain groups. These changes could make IDR plans a more attractive and effective path to debt relief for a wider range of borrowers.

the save plan and future idr innovations

The Saving on a Valuable Education (SAVE) plan, for instance, calculates payments based on a smaller percentage of discretionary income and includes provisions for interest subsidies, preventing loan balances from growing due to unpaid interest. These features are revolutionary and set a new standard for IDR plans.

- Lower monthly payments: Based on a smaller portion of discretionary income.

- Interest subsidy: Prevents unpaid interest from accruing, stopping balance growth.

- Faster forgiveness: Forgiveness timelines shortened for certain loan amounts.

Looking ahead to 2026, policymakers may consider further innovations within the IDR framework. This could include automatic enrollment for eligible borrowers, more simplified annual recertification processes, or even targeted relief for specific professions or economic backgrounds. The goal is to ensure that IDR plans genuinely serve as a safety net, protecting borrowers from default and providing a clear path to eventual debt freedom.

targeted forgiveness programs and special considerations

Beyond broad federal programs, several targeted forgiveness initiatives address specific professional fields or unique circumstances. These programs, which are often less publicized, can offer significant relief for eligible individuals. For 2026, it’s crucial for borrowers to research these niche programs, as they might provide a faster or more direct route to forgiveness based on their career choices or personal situations.

Examples include programs for teachers, nurses, doctors practicing in underserved areas, and individuals working in specific research fields. While the general eligibility requirements for these programs are well-established, there may be updates or new offerings in 2026 that expand their scope or simplify the application process. Staying informed about these specialized options can open up unexpected avenues for debt relief.

exploring profession-specific relief

Many states also offer their own loan forgiveness or repayment assistance programs for professionals who commit to working in high-need areas or specific fields within their state. These state-level programs can often be combined with federal benefits, maximizing the potential for debt reduction. It’s essential to check both federal and state resources.

- Teacher Loan Forgiveness: For teachers in low-income schools for five consecutive years.

- Nurse Corps Loan Repayment Program: For registered nurses and nurse faculty working in critical shortage facilities.

- Perkins Loan Cancellation: For various public service professions, depending on the percentage of service.

Furthermore, special considerations for borrowers with disabilities or those who have had their schools close are also important. These specific situations often have unique forgiveness pathways designed to provide relief when conventional repayment is not feasible. As with all forgiveness programs, thorough research and understanding of the specific criteria are paramount.

application processes and documentation for 2026 forgiveness

Successfully applying for student loan forgiveness requires meticulous attention to detail and a clear understanding of the necessary documentation. While specific forms and submission methods may evolve by 2026, the fundamental requirement for accurate and timely submission of information will remain. Borrowers should begin gathering relevant documents well in advance of applying to ensure a smooth process.

This includes employment verification forms, income documentation, and records of past payments. The Department of Education and federal loan servicers are continually working to streamline these processes, but the onus is ultimately on the borrower to provide all requested information correctly. Errors or omissions can lead to significant delays or even denial of forgiveness.

essential documentation and tips for a smooth application

Maintaining organized records throughout your repayment journey is invaluable. This includes keeping copies of all loan statements, payment confirmations, and any correspondence with your loan servicer. For PSLF, regularly submitting the Employment Certification Form (ECF) is crucial, even if not yet eligible for forgiveness, as it helps track qualifying payments.

- Proof of employment: Employer certification forms, pay stubs, and tax documents.

- Income verification: Tax returns (IRS Form 1040) and recent pay stubs.

- Loan statements: Records from your loan servicer detailing payments and loan status.

As 2026 approaches, it is advisable to check the official Federal Student Aid (FSA) website for the most current application forms and instructions. Many applications can now be completed online, making the process more efficient. However, always double-check that you are using the most recent version of any form and submitting it through the approved channels.

preparing for student loan forgiveness: strategies for borrowers

Even with the promise of new pathways and expanded eligibility, proactive preparation remains key to successfully navigating student loan forgiveness programs in 2026. Borrowers should not wait until the last minute to understand their options, assess their eligibility, and make strategic decisions about their repayment plans. Early planning can make a significant difference in the amount of debt relief ultimately received.

This preparation involves more than just gathering documents; it includes understanding your loan types, consolidating if necessary, enrolling in appropriate repayment plans, and staying informed about policy changes. A well-thought-out strategy can optimize your path to forgiveness and ensure you meet all necessary criteria when the time comes to apply.

actionable steps for debt relief

One of the most important steps is to know your loan portfolio inside and out. Different loan types (e.g., FFEL, Perkins, Direct Loans) have different rules regarding forgiveness. Consolidating older federal loans into a Direct Consolidation Loan can be a crucial step for making them eligible for programs like PSLF or IDR forgiveness.

- Understand your loan types: Differentiate between federal and private loans.

- Consider loan consolidation: To make certain loans eligible for more programs.

- Choose the right repayment plan: Select an IDR plan that aligns with your financial situation and forgiveness goals.

Regularly checking your loan status with your servicer and the Federal Student Aid website is also vital. These platforms provide personalized information about your loans, payment history, and progress towards forgiveness. By taking these proactive steps, borrowers can position themselves to take full advantage of the opportunities presented by student loan forgiveness programs in 2026.

| Key Program | Brief Description |

|---|---|

| Public Service Loan Forgiveness (PSLF) | Forgiveness for direct loans after 120 qualifying payments in public service. |

| Income-Driven Repayment (IDR) Plans | Payments based on income, with remaining balance forgiven after 20-25 years. |

| SAVE Plan | Newest IDR option with lower payments and interest subsidies, preventing balance growth. |

| Targeted Forgiveness | Specific programs for professions like teachers, nurses, and those in underserved areas. |

frequently asked questions about student loan forgiveness 2026

For 2026, expect expanded eligibility criteria for existing programs like PSLF and IDR, potentially simplified application processes, and new considerations for economic hardship. The SAVE plan, introduced recently, sets a precedent for more borrower-friendly IDR options with lower payments and interest subsidies.

Qualifying employment for PSLF generally includes full-time work for government organizations (federal, state, local, tribal) or 501(c)(3) non-profit organizations. It’s crucial to submit the PSLF Employment Certification Form regularly to ensure your employer and payments are being tracked correctly by your loan servicer.

No, federal student loan forgiveness programs, including PSLF and IDR plans, only apply to federal student loans. Private student loans are issued by banks or private lenders and do not qualify for these federal relief options. Borrowers with private loans should explore refinancing or other private relief options.

The Saving on a Valuable Education (SAVE) plan is an Income-Driven Repayment plan that calculates monthly payments based on a lower percentage of discretionary income. A key benefit is its interest subsidy, which prevents your loan balance from growing due to unpaid interest, even if your payment is $0.

Start by understanding your loan types, and consider consolidating federal loans if needed. Enroll in an appropriate IDR plan, like SAVE, and regularly certify your employment for PSLF if applicable. Stay updated on official announcements from the Department of Education and keep meticulous records.

conclusion

The landscape of student loan forgiveness programs in 2026 is poised to offer significant opportunities for borrowers seeking debt relief. With anticipated enhancements to existing programs like PSLF and IDR, alongside potential new targeted initiatives, the pathway to financial freedom from student debt may become clearer and more accessible. Proactive engagement, diligent record-keeping, and continuous monitoring of official guidance will be paramount for borrowers aiming to leverage these evolving programs effectively. By staying informed and strategic, millions of Americans can look forward to a future with reduced or eliminated student loan burdens, fostering greater economic stability and opportunity.