2026 Social Security Benefits: Unpacking the 3.2% COLA Increase

Anúncios

The 3.2% Cost-of-Living Adjustment (COLA) for 2026 Social Security benefits will directly increase monthly payouts for eligible retirees and beneficiaries, aiming to offset inflation and maintain purchasing power.

Understanding the 2026 Social Security Benefits, particularly what the 3.2% COLA increase means for your payouts, is crucial for anyone relying on these funds. As we approach 2026, millions of Americans are eager to grasp how this adjustment will influence their financial well-being, especially amidst ongoing economic shifts. This article delves into the intricacies of Social Security, the impact of the Cost-of-Living Adjustment, and what beneficiaries can expect.

Anúncios

The Basics of Social Security Benefits

Social Security has been a cornerstone of American retirement planning for decades, providing financial support to retirees, disabled workers, and survivors. It’s a complex system, funded primarily through payroll taxes, and designed to offer a safety net for those who have contributed throughout their working lives. Understanding its fundamental principles is the first step toward appreciating the significance of any adjustments.

Anúncios

Who is Eligible for Social Security?

Eligibility for Social Security benefits is determined by a system of work credits. Most individuals need to accumulate 40 credits over their working career, with a maximum of four credits earned per year. This typically translates to 10 years of work. These credits establish your right to future benefits, but the amount you receive depends on several other factors.

- Retirement Age: Your full retirement age (FRA) varies based on your birth year, impacting when you can claim unreduced benefits.

- Earnings History: Your average indexed monthly earnings (AIME) over your 35 highest-earning years are used to calculate your primary insurance amount (PIA).

- Type of Benefit: Benefits extend beyond just retirement, covering disability, survivor benefits, and spousal benefits, each with specific eligibility criteria.

The system is designed to be progressive, meaning lower-income workers receive a higher percentage of their pre-retirement earnings in benefits compared to higher-income workers. This aims to provide a more equitable distribution of aid. Navigating these rules can be challenging, but understanding your personal earnings record and projected benefits is vital for effective financial planning.

In essence, Social Security benefits are a promise of financial security in later life, built upon contributions made during your working years. The program’s stability and ability to adapt to economic changes are frequently debated, making every annual adjustment a point of significant interest for beneficiaries and future retirees.

Understanding the Cost-of-Living Adjustment (COLA)

The Cost-of-Living Adjustment, or COLA, is a critical component of Social Security, designed to ensure that the purchasing power of benefits is not eroded by inflation. Each year, the Social Security Administration (SSA) reviews economic data to determine if an adjustment is necessary. This mechanism is vital for maintaining the financial stability of retirees and other beneficiaries.

How COLA is Calculated

COLA is primarily based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). Specifically, the SSA compares the average CPI-W for the third quarter of the current year (July, August, and September) with the average for the third quarter of the last year in which a COLA was determined. If there’s an increase, that percentage becomes the COLA for the upcoming year.

- CPI-W as a Benchmark: This index measures changes in the prices of goods and services purchased by urban wage earners and clerical workers.

- Annual Review: The review process is annual, ensuring that benefits keep pace with the cost of living.

- No Negative COLA: By law, Social Security benefits cannot decrease due to a COLA. If the CPI-W shows no increase, there is no COLA for that year.

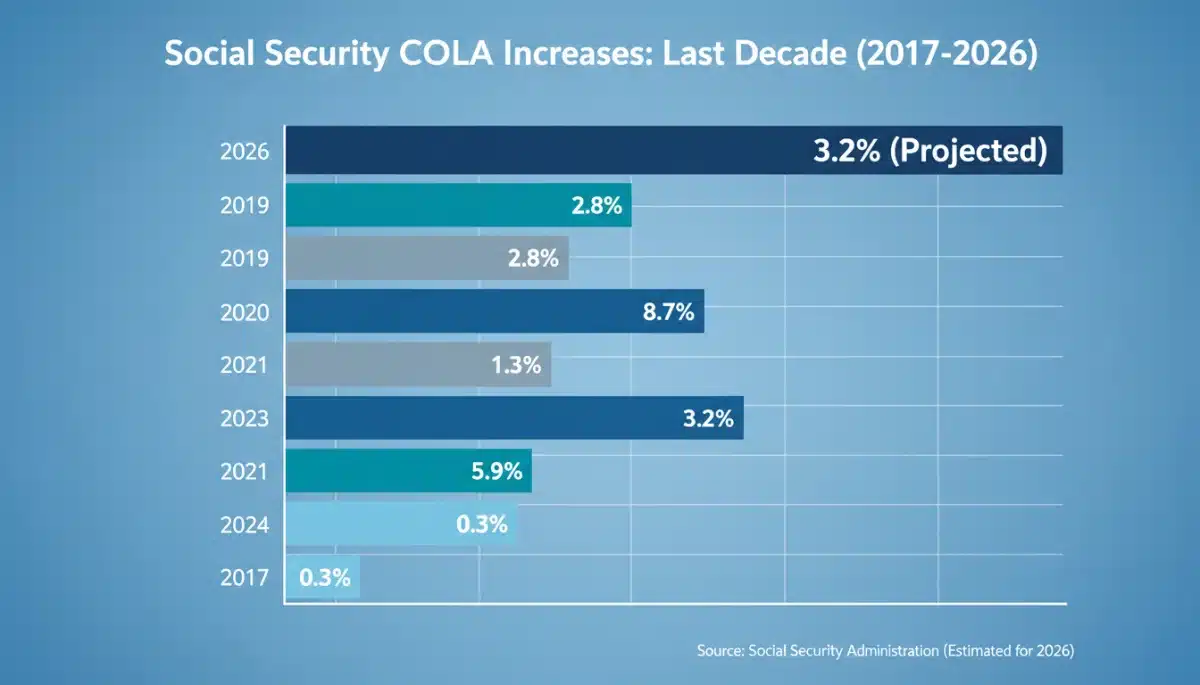

The 3.2% COLA for 2026 reflects the inflationary pressures experienced in the preceding period. This adjustment is a direct response to rising costs for everyday necessities, from groceries to utilities. Without COLA, beneficiaries would find their fixed incomes diminishing in real value over time, making it harder to cover essential expenses.

The calculation method ensures that beneficiaries receive an increase that is directly tied to changes in consumer prices, providing a measure of economic stability. While the CPI-W is specifically for urban wage earners and clerical workers, it serves as a representative measure for the broader population of Social Security beneficiaries.

The 3.2% COLA Increase for 2026: What It Means

The announcement of a 3.2% COLA increase for 2026 is significant news for millions of Americans. This adjustment will directly translate into higher monthly benefit checks, providing much-needed relief against the backdrop of persistent inflation. It’s not just a number; it represents a tangible boost in purchasing power for those who rely on Social Security.

Impact on Monthly Payouts

For an average retiree receiving, for example, $1,800 per month, a 3.2% COLA would add approximately $57.60 to their monthly check, bringing it to $1,857.60. While this might seem modest to some, for many beneficiaries, every dollar makes a difference in covering rising expenses like food, housing, and healthcare.

- Increased Purchasing Power: The primary goal is to help beneficiaries maintain their standard of living.

- Varies by Individual: The exact dollar increase will depend on each individual’s current benefit amount.

- Applies to All Benefit Types: Retirement, disability, and survivor benefits will all see this increase.

This increase also affects the maximum Social Security benefit. For those who earned the maximum taxable amount throughout their careers and claim benefits at their full retirement age, the new COLA will push their monthly payouts even higher. This helps ensure that even high earners see their benefits adjusted for inflation.

Beyond the immediate financial boost, the 3.2% COLA also signals the SSA’s commitment to protecting beneficiaries from the erosive effects of inflation. It’s a reminder that the system is designed to be dynamic, adapting to economic realities to fulfill its promise of financial security.

Navigating Increased Benefits and Financial Planning

While a 3.2% COLA increase for 2026 is certainly welcome, it also brings considerations for personal financial planning. Maximizing the impact of these increased benefits requires careful thought, especially regarding budgeting, taxes, and potential impacts on other income sources. Proactive planning can help ensure these adjustments truly enhance your financial security.

Budgeting with the New COLA

The extra funds can be allocated strategically. For some, it might mean covering rising healthcare costs or utility bills. For others, it could be an opportunity to build a stronger emergency fund or reduce small debts. It’s essential to review your current budget and see where the additional income can have the most positive effect.

- Review Expenses: Reassess your monthly expenditures to identify areas where the COLA can provide relief.

- Prioritize Needs: Focus on essential costs before considering discretionary spending.

- Save or Invest: If possible, consider saving or investing a portion of the increased benefit for future needs.

It’s also important to be aware that increased Social Security benefits can sometimes lead to higher tax liabilities. If your combined income (adjusted gross income plus non-taxable interest plus one-half of your Social Security benefits) exceeds certain thresholds, a portion of your benefits may become taxable. Understanding these thresholds is crucial for tax planning.

Furthermore, for those receiving other government benefits, an increase in Social Security payments could potentially affect eligibility or benefit amounts for income-tested programs. It is advisable to consult with a financial advisor or the relevant agency to understand any potential implications. Strategic financial planning ensures that the COLA increase genuinely improves your overall financial standing without unexpected drawbacks.

Potential Challenges and Future Outlook

While the 3.2% COLA for 2026 offers immediate relief, it’s also important to consider the broader context of Social Security’s long-term financial health and the challenges it faces. Understanding these dynamics can help beneficiaries and future retirees prepare for potential future changes and plan accordingly.

Inflationary Pressures and Program Solvency

The very reason for COLA—inflation—also poses a challenge. Sustained high inflation can put pressure on the Social Security trust funds. While COLA helps beneficiaries keep pace, it also increases the program’s expenditures. The long-term solvency of Social Security is a recurring topic of discussion, with various proposals for reforms.

- Trust Fund Projections: The Social Security and Medicare Boards of Trustees regularly release reports on the financial status of the programs.

- Demographic Shifts: An aging population and lower birth rates mean fewer workers supporting more retirees, straining the system.

- Potential Reforms: Discussions around increasing the full retirement age, adjusting the COLA calculation, or raising the payroll tax cap are ongoing.

For beneficiaries, these discussions highlight the importance of not solely relying on Social Security for retirement income. Diversifying income streams through personal savings, investments, and pensions remains a critical strategy for financial security. The 3.2% COLA is a positive development, but it shouldn’t overshadow the need for comprehensive financial planning.

Looking ahead, the future of Social Security will likely involve continued adjustments and possibly reforms to ensure its sustainability for future generations. Staying informed about these discussions and understanding their potential impact on your benefits is an essential part of responsible financial management.

Maximizing Your Social Security Benefits Beyond COLA

Beyond the annual COLA, there are several strategic decisions individuals can make to maximize their Social Security benefits. These choices, often made years before retirement, can significantly impact the total amount received over a lifetime. Understanding these options is key to a robust retirement plan.

Strategic Claiming Age

One of the most impactful decisions is when to start claiming benefits. While you can start as early as age 62, your monthly benefit will be permanently reduced. Waiting until your full retirement age (FRA) allows you to receive 100% of your primary insurance amount. Delaying even further, up to age 70, can earn you delayed retirement credits, increasing your monthly benefit by up to 8% per year beyond your FRA.

- Early Claiming: Reduces monthly benefits but provides income sooner.

- Full Retirement Age: Receives 100% of earned benefits.

- Delayed Claiming: Increases monthly benefits significantly, up to age 70.

The decision to claim early, at FRA, or to delay depends on individual circumstances, including health, other income sources, and financial needs. For a healthy individual with other retirement savings, delaying benefits can be a powerful strategy to ensure a higher guaranteed income stream later in life.

Reviewing Your Earnings Record

It’s also crucial to regularly review your Social Security earnings record for accuracy. Errors can occur, and correcting them can ensure your benefit calculation is based on your complete and correct work history. You can access your earnings record through your personal My Social Security account online.

By taking an active role in understanding and planning for Social Security, individuals can ensure they are making the most of this vital program. The 3.2% COLA for 2026 is a welcome boost, but it’s just one piece of the larger puzzle of comprehensive retirement financial planning.

| Key Aspect | Description |

|---|---|

| 2026 COLA Increase | Social Security benefits to increase by 3.2% due to Cost-of-Living Adjustment. |

| Impact on Payouts | Directly boosts monthly checks, helping maintain purchasing power against inflation. |

| COLA Calculation | Based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). |

| Financial Planning | Review budgeting, tax implications, and consider strategic claiming age for optimal benefits. |

Frequently Asked Questions About 2026 Social Security Benefits

The 3.2% COLA means your monthly Social Security benefit payment will increase by 3.2% starting January 2026. For example, if your current benefit is $1,500, it will increase by $48, bringing your new payment to $1,548.

The COLA is determined by comparing the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) from the third quarter of the current year to the third quarter of the last year a COLA was enacted. An increase results in a COLA for the next calendar year.

Yes, an increase in your Social Security benefits could potentially push your combined income above certain thresholds, making a larger portion of your benefits subject to federal income tax. It’s advisable to consult a tax professional.

Yes, the Cost-of-Living Adjustment applies to all types of Social Security benefits, including retirement, disability (SSDI), and survivor benefits. Everyone receiving Social Security payments will see their benefit amount adjusted by the 3.2% increase.

Beyond COLA, your benefit amount is influenced by your average indexed monthly earnings over your 35 highest-earning years, your full retirement age, and the age at which you choose to start claiming benefits. Strategic claiming can significantly impact your total lifetime benefits.

Conclusion

The 3.2% COLA increase for 2026 Social Security benefits is a crucial development for millions of Americans, directly impacting their financial stability and purchasing power. While it provides a welcome boost to monthly payouts, it also underscores the importance of a holistic approach to retirement planning. Beneficiaries should carefully consider how this adjustment fits into their overall financial strategy, accounting for budgeting, potential tax implications, and the broader economic landscape. Staying informed and making proactive decisions remains key to maximizing the benefits of Social Security and securing a comfortable financial future.