New Homebuyer Assistance Programs 2026: Federal Benefits for First-Time Buyers

Anúncios

New federal homebuyer assistance programs in 2026 will introduce enhanced benefits and support mechanisms specifically designed to empower first-time buyers in achieving their homeownership aspirations nationwide.

Are you dreaming of owning your first home in 2026 but feel overwhelmed by the financial hurdles? The good news is that new federal initiatives are on the horizon, promising to make homeownership a more tangible reality for many. Understanding the latest New Homebuyer Assistance Programs in 2026: Federal Benefits for First-Time Buyers is your first step toward unlocking the door to your future home.

Anúncios

Understanding the Evolving Landscape of Federal Homebuyer Programs

The housing market is constantly shifting, and with it, the support structures designed to help first-time homebuyers. In 2026, the federal government is introducing several updated and new programs aimed at addressing current economic realities and making homeownership more accessible. These initiatives reflect a commitment to fostering stable communities and empowering individuals to build equity.

Anúncios

Navigating these programs can seem complex, but understanding their core objectives and eligibility requirements is crucial. Many programs focus on reducing upfront costs, such as down payments and closing costs, which are often the biggest barriers for new buyers. Others aim to lower monthly mortgage payments through favorable interest rates or tax credits.

Key Changes and New Initiatives for 2026

- Expanded Eligibility Criteria: Some programs are broadening their income limits and geographic scope to reach more diverse populations.

- Increased Grant Amounts: Federal grants for down payment assistance are seeing an uptick, providing more significant financial relief.

- Streamlined Application Processes: Efforts are being made to simplify the application process, making it less daunting for first-time applicants.

These changes are designed to be more responsive to the needs of today’s homebuyers, offering a more robust safety net and clearer pathways to securing a home. Staying informed about these updates will give you a significant advantage in your homebuying journey.

In essence, the 2026 landscape for federal homebuyer programs is characterized by greater inclusivity and enhanced financial support. This evolution is a direct response to challenges faced by prospective homeowners, ensuring that the dream of owning a home remains within reach for a broader segment of the population.

Exploring Federal Housing Administration (FHA) Loan Enhancements

The Federal Housing Administration (FHA) loan program remains a cornerstone of federal assistance for first-time homebuyers, and 2026 brings several enhancements designed to further its effectiveness. FHA loans are renowned for their low down payment requirements and more flexible credit standards, making them particularly attractive to those who might not qualify for conventional mortgages.

These loans are insured by the FHA, protecting lenders against borrower default and thus encouraging them to offer more favorable terms to a wider range of applicants. The recent adjustments aim to strengthen this foundation, ensuring FHA loans continue to serve as a vital resource for entry-level homeownership.

Updated FHA Loan Requirements and Benefits

- Lower Mortgage Insurance Premiums (MIP): While FHA loans require both upfront and annual mortgage insurance, there are discussions around potential adjustments to these premiums to reduce the overall cost of homeownership.

- Increased Loan Limits: FHA loan limits are periodically updated to reflect changes in housing costs across different regions, allowing buyers to finance more expensive homes in high-cost areas.

- Flexible Underwriting for Student Debt: Recognizing the burden of student loans, new guidelines may offer more flexibility in how student debt is assessed during the underwriting process, potentially easing the path for younger buyers.

These enhancements are critical for maintaining the FHA’s relevance and impact in a dynamic housing market. They underscore a commitment to making homeownership attainable, especially for those with moderate incomes or less-than-perfect credit histories.

The FHA program in 2026 continues its legacy of providing a crucial pathway to homeownership for many Americans. By focusing on reduced financial barriers and accommodating modern financial challenges, FHA loans remain an indispensable tool for first-time buyers.

Veterans Affairs (VA) Loans: Specialized Benefits for Service Members

For eligible service members, veterans, and their spouses, VA loans represent one of the most powerful and comprehensive homebuyer assistance programs available. These loans, guaranteed by the Department of Veterans Affairs, offer unparalleled benefits, most notably the ability to purchase a home with no down payment and without private mortgage insurance (PMI). In 2026, the VA loan program continues to be a beacon for those who have served our nation.

The program’s structure is designed to acknowledge the unique financial situations and sacrifices made by military personnel. Beyond the zero down payment, VA loans often come with competitive interest rates and limited closing costs, significantly reducing the financial burden of buying a home. This makes them an incredibly valuable resource for the veteran community.

Key Advantages and Updates for VA Loan Beneficiaries

- No Down Payment Requirement: This remains a hallmark of VA loans, allowing eligible buyers to finance 100% of their home’s purchase price.

- No Private Mortgage Insurance (PMI): Unlike conventional loans with less than 20% down, VA loans do not require PMI, which can save borrowers hundreds of dollars monthly.

- Competitive Interest Rates: VA loans typically offer some of the lowest interest rates on the market, thanks to the government guarantee.

- Funding Fee Exemptions: Certain veterans, particularly those receiving VA disability compensation, may be exempt from paying the VA funding fee, further reducing upfront costs.

These benefits collectively make VA loans an exceptionally attractive option for military members and veterans. The 2026 outlook continues to emphasize the government’s commitment to providing robust housing support for those who have dedicated their lives to service.

The VA loan program consistently stands out for its comprehensive support, enabling military families to achieve homeownership with significant financial advantages. These specialized benefits underscore the nation’s gratitude and commitment to its service members.

USDA Rural Development Loans: Supporting Homeownership in Rural Areas

For individuals and families looking to purchase a home in designated rural areas, the USDA Rural Development loan program offers another powerful avenue for achieving homeownership. These loans, backed by the U.S. Department of Agriculture, are designed to promote economic growth and improve the quality of life in rural communities by providing affordable housing options. Similar to VA loans, eligible borrowers can often purchase a home with no money down, making it an excellent option for those in qualifying areas.

The USDA loan program is not just for agricultural workers; it serves a broad spectrum of individuals seeking to live in rural or suburban areas that meet specific population and geographic criteria. In 2026, the program continues its mission to expand access to safe and affordable housing outside of major metropolitan centers.

Eligibility and Benefits of USDA Loans in 2026

- Zero Down Payment: A significant advantage, allowing buyers to finance 100% of the home’s purchase price.

- Flexible Credit Requirements: While credit is assessed, USDA loans often have more lenient guidelines compared to conventional mortgages.

- Competitive Interest Rates: The government backing helps secure favorable interest rates for borrowers.

- Income Limitations: Eligibility is tied to income limits, which vary by location and household size, ensuring the program serves those who genuinely need assistance.

- Designated Rural Areas: Properties must be located in eligible rural areas, which are updated periodically by the USDA.

These aspects make USDA loans a unique and valuable resource for promoting homeownership in less densely populated regions. The program’s focus on rural development helps to balance housing opportunities across the country.

The USDA Rural Development loan program remains a crucial tool for fostering homeownership and community development in rural America. Its zero-down payment option and favorable terms continue to make it an attractive choice for eligible buyers.

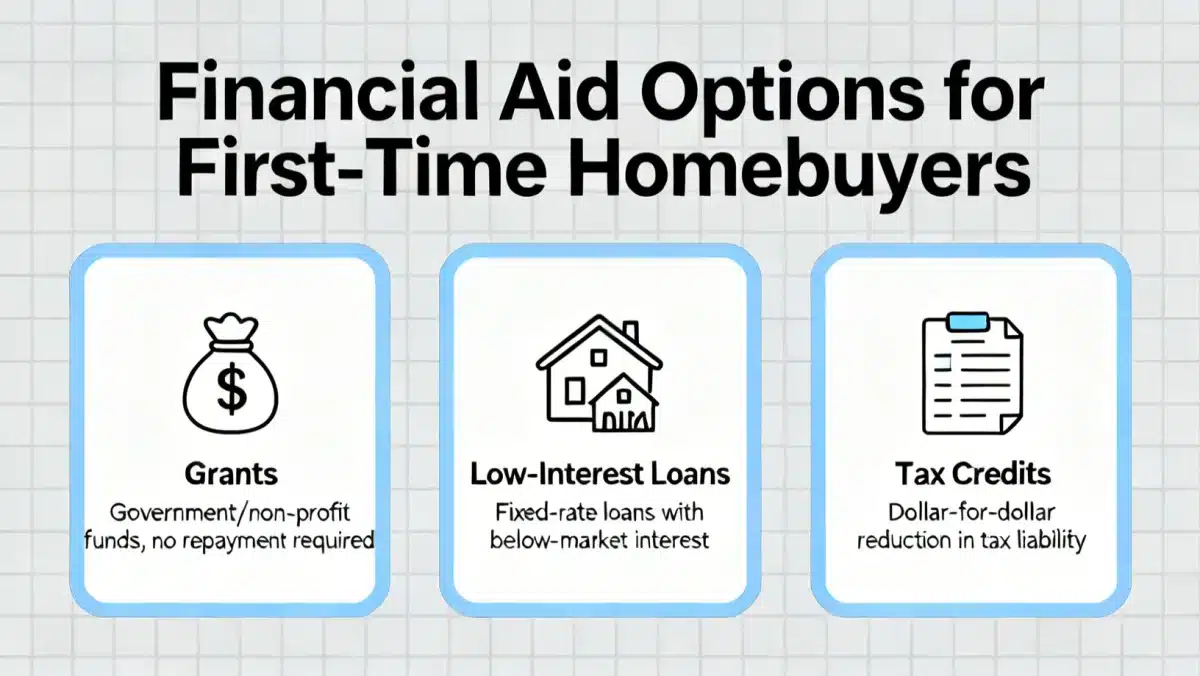

Federal Grants and Down Payment Assistance Programs

Beyond traditional loan programs, a variety of federal grants and down payment assistance programs are available to help first-time homebuyers overcome the initial financial hurdles of purchasing a home. These programs often work in conjunction with FHA, VA, or USDA loans, providing funds that do not need to be repaid or offering low-interest loans specifically for down payments and closing costs. In 2026, the emphasis on making homeownership more attainable means these grant programs are more vital than ever.

Many of these grants are administered at the state or local level, often funded by federal initiatives like the HOME Investment Partnerships Program or Community Development Block Grants (CDBG). They are designed to assist low-to-moderate income individuals and families, making the dream of homeownership a reality by significantly reducing the upfront cash needed.

Types of Federal Grants and Assistance

- Down Payment Assistance (DPA): These programs provide funds to cover part or all of the required down payment, often structured as deferred loans, forgivable loans, or outright grants.

- Closing Cost Assistance: Some programs specifically target closing costs, which can add thousands of dollars to the home purchase price.

- First-Time Homebuyer Tax Credits: While not a direct grant, federal tax credits can reduce a homebuyer’s tax liability, effectively putting money back in their pocket.

- Housing Counseling Services: Many federal programs require or recommend housing counseling, which helps buyers understand the homebuying process and financial responsibilities.

Accessing these grants often involves meeting specific income, residency, and first-time homebuyer criteria. It is essential to research programs available in your specific state or locality, as offerings can vary widely.

Federal grants and down payment assistance programs are indispensable for bridging the financial gap for many first-time buyers. They represent a significant commitment to ensuring that initial costs do not permanently bar aspiring homeowners from the market.

Navigating the Application Process and Eligibility

Successfully accessing New Homebuyer Assistance Programs in 2026: Federal Benefits for First-Time Buyers requires a clear understanding of the application process and eligibility criteria. While specific requirements vary by program, there are common threads that prospective homebuyers should be aware of. Preparation is key to a smooth and successful application journey.

The first step typically involves assessing your financial readiness and understanding which programs you might qualify for. This often means gathering financial documents, checking your credit score, and determining your household income. Many federal programs are designed for first-time buyers, generally defined as someone who has not owned a home in the past three years.

Key Steps and Considerations for Applicants

- Credit Score Review: While some federal loans are more flexible, a good credit score can unlock better terms and more program options. Understand what your score is and how to improve it if necessary.

- Income and Debt-to-Income Ratio: Most programs have income limits and evaluate your debt-to-income ratio to ensure you can afford the mortgage payments.

- First-Time Homebuyer Definition: Confirm you meet the definition of a first-time homebuyer, which is crucial for many assistance programs.

- Required Documentation: Be prepared to provide extensive documentation, including pay stubs, tax returns, bank statements, and identification.

- Housing Counseling: Some programs mandate participation in a homebuyer education course or counseling, which can be immensely beneficial.

Working with a knowledgeable lender who specializes in federal loan programs can significantly streamline the process. They can help you identify the best-fit programs and guide you through the intricacies of the application.

Understanding and carefully navigating the application process is paramount for first-time buyers. By addressing eligibility requirements and preparing necessary documentation, applicants can effectively utilize federal programs to achieve homeownership.

Future Outlook: Sustaining Homeownership Accessibility

The landscape of New Homebuyer Assistance Programs in 2026: Federal Benefits for First-Time Buyers is not static; it reflects an ongoing commitment to sustaining and expanding homeownership accessibility. As economic conditions and housing market dynamics continue to evolve, federal programs are likely to adapt further, ensuring they remain relevant and effective for future generations of homebuyers. The long-term goal is to create a more equitable housing market where the dream of owning a home is within reach for a broader segment of the population, fostering economic stability and community growth.

Policymakers are continually evaluating the impact of existing programs and exploring new strategies to address challenges such as rising home prices, interest rate fluctuations, and the persistent need for affordable housing. This forward-looking approach suggests that while the specific details of programs may change, the underlying federal support for first-time homebuyers will likely endure and potentially expand.

Anticipated Trends and Continued Support

- Focus on Sustainable Homeownership: Programs may increasingly integrate components that support long-term home retention and financial literacy, not just the initial purchase.

- Technological Integration: Expect more digital tools and platforms to simplify the application and information-gathering processes, making programs more user-friendly.

- Targeted Assistance for Underserved Communities: There may be an increased emphasis on tailoring programs to meet the specific needs of historically underserved communities, addressing systemic barriers to homeownership.

- Partnerships with Non-Profits and Local Governments: Enhanced collaboration between federal agencies and local entities could lead to more localized and effective assistance programs.

These trends indicate a proactive stance by the federal government to ensure that homeownership remains a viable goal. For prospective first-time buyers, this means continued opportunities and evolving support mechanisms designed to help them navigate the complexities of the housing market.

The future of federal homebuyer assistance programs appears robust, with an ongoing commitment to adaptability and inclusivity. These efforts are crucial for sustaining homeownership accessibility and ensuring that federal benefits continue to empower first-time buyers.

| Program Type | Key Benefit for First-Time Buyers |

|---|---|

| FHA Loans | Low down payment (as low as 3.5%), flexible credit requirements. |

| VA Loans | No down payment, no PMI, competitive interest rates for veterans. |

| USDA Loans | Zero down payment for eligible rural properties and income levels. |

| Down Payment Grants | Non-repayable funds to cover down payment and/or closing costs. |

Frequently Asked Questions About 2026 Homebuyer Programs

Generally, a ‘first-time homebuyer’ is an individual who has not owned a primary residence in the past three years. This definition can sometimes include individuals who have owned a home previously but whose spouse has not, or those who have only owned a non-permanent structure.

While many programs prioritize low-to-moderate income individuals, not all federal assistance is exclusively for them. Programs like FHA loans have broader income eligibility, and VA loans are based on military service, not income. It’s crucial to check specific program requirements.

Yes, it is often possible to combine different federal and state/local programs. For example, an FHA loan can be paired with a down payment assistance grant. However, there might be specific rules and limitations, so consulting with a qualified lender is highly recommended.

Your credit score is a significant factor. While some federal programs like FHA loans are more lenient, a higher score generally leads to better interest rates and more favorable terms. It’s advisable to check and improve your credit score before applying.

The best resources are the official websites of federal agencies like HUD, VA, and USDA. Additionally, state housing finance agencies (HFA) and local housing authorities often have comprehensive lists of programs available in your specific geographic region.

Conclusion

The array of New Homebuyer Assistance Programs in 2026: Federal Benefits for First-Time Buyers presents unparalleled opportunities for aspiring homeowners across the United States. From the flexible terms of FHA loans to the zero-down payment options of VA and USDA programs, and the invaluable support of federal grants, the pathway to homeownership is more accessible than ever. By understanding these vital resources, diligently preparing for the application process, and seeking expert guidance, first-time buyers can confidently navigate the housing market and turn their dream of owning a home into a tangible reality.