HSAs in 2026: Maximizing Tax-Free Growth by 12% Annually

Anúncios

Health Savings Accounts (HSAs) in 2026 are poised to offer unprecedented opportunities for maximizing tax-free growth, serving as a critical financial instrument for healthcare and retirement savings.

Are you looking for a powerful financial tool that not only covers your healthcare costs but also supercharges your retirement savings? In 2026, Health Savings Accounts (HSAs) continue to stand out as an exceptional vehicle for maximizing tax-free growth, potentially up to 12% annually. This comprehensive guide will delve into how HSAs work, their unparalleled tax advantages, and strategic ways to leverage them for both immediate medical expenses and long-term financial security.

Anúncios

Understanding Health Savings Accounts (HSAs) in 2026

Health Savings Accounts (HSAs) are tax-advantaged savings accounts available to those who have a High-Deductible Health Plan (HDHP). They are designed to help individuals save for qualified medical expenses on a tax-free basis. In 2026, the core principles of HSAs remain steadfast, offering a unique blend of healthcare coverage and investment potential.

Anúncios

Eligibility for an HSA is tied directly to enrollment in an HDHP. These plans feature higher deductibles than traditional health insurance plans but typically come with lower monthly premiums. This structure encourages individuals to be more mindful of their healthcare spending, while the HSA provides a mechanism to save and pay for those higher out-of-pocket costs.

Eligibility Requirements for HSAs

To be eligible for an HSA in 2026, you must meet specific criteria set by the IRS. These requirements ensure that HSAs are utilized as intended – for individuals taking on more responsibility for their healthcare costs through an HDHP.

- High-Deductible Health Plan (HDHP): You must be covered by a qualifying HDHP. For 2026, the IRS typically adjusts the minimum deductible and maximum out-of-pocket limits for HDHPs.

- No Other Health Coverage: Generally, you cannot be covered by any other health plan that is not an HDHP, with some exceptions for specific types of limited coverage.

- Not Enrolled in Medicare: Individuals enrolled in Medicare are not eligible to contribute to an HSA.

- Not Claimed as a Dependent: You cannot be claimed as a dependent on someone else’s tax return.

Understanding these eligibility rules is the first step toward unlocking the significant financial benefits an HSA offers. Staying informed about the annual adjustments to HDHP definitions is crucial for continuous eligibility.

The flexibility of HSAs extends beyond just paying for immediate medical needs. The funds within an HSA can be invested, allowing them to grow over time, similar to a retirement account. This investment component is where much of the long-term tax-free growth potential lies, making HSAs a dual-purpose financial tool for both health and wealth.

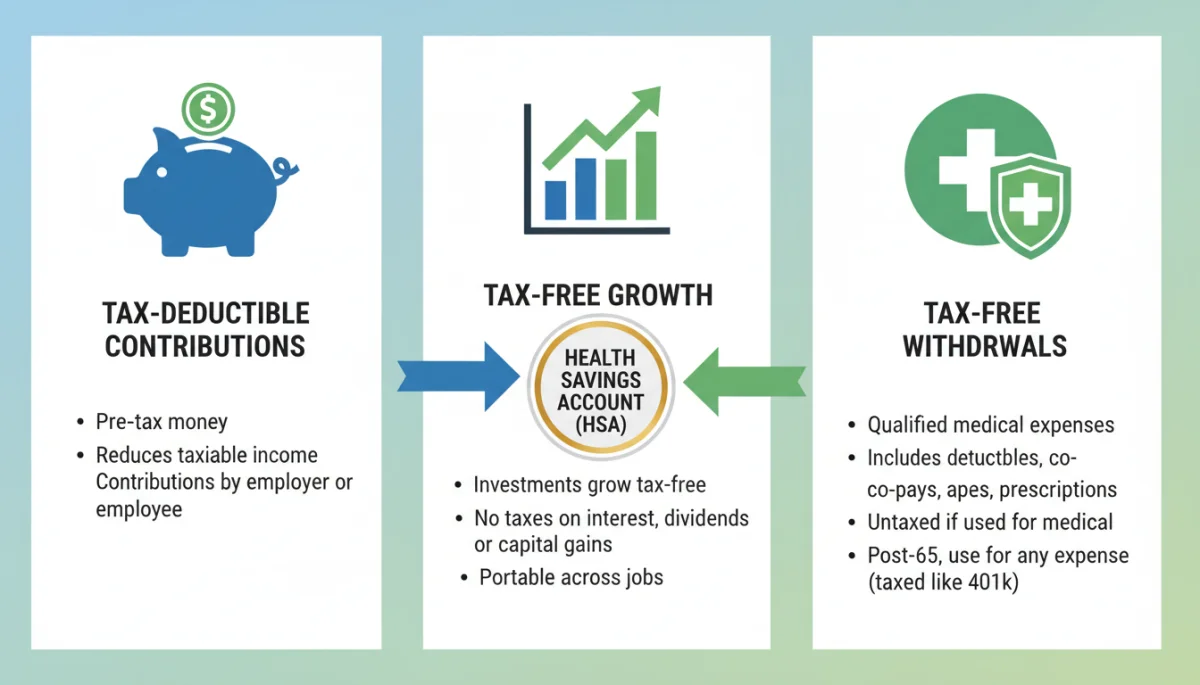

The Triple-Tax Advantage: A Cornerstone of HSA Growth

The true power of Health Savings Accounts (HSAs) lies in their unparalleled triple-tax advantage, a feature that distinguishes them from almost any other savings or investment vehicle. This triple benefit provides significant tax savings throughout the lifecycle of your HSA funds, from contribution to withdrawal.

Firstly, contributions made to an HSA are tax-deductible. This means that the money you put into your HSA reduces your taxable income for the year, leading to immediate tax savings. Whether you contribute directly from your paycheck or make personal contributions, these amounts are subtracted from your gross income, lowering your overall tax liability.

Tax-Deductible Contributions

The ability to contribute pre-tax dollars or deduct post-tax contributions is a significant advantage. This immediately lowers your taxable income, reducing your current year’s tax burden. Many employers facilitate this by allowing pre-tax contributions directly from payroll, simplifying the process and ensuring you receive the tax benefit upfront.

Tax-Free Growth

Perhaps the most compelling aspect of an HSA, especially when considering long-term financial planning, is the tax-free growth of your investments. Once funds are in your HSA, you can often invest them in a variety of options, such as mutual funds, stocks, or bonds, depending on your HSA provider. Any capital gains, dividends, or interest earned on these investments grow free from federal income tax. This compounding effect over many years can lead to substantial wealth accumulation, far exceeding what would be possible in a taxable account.

Tax-Free Withdrawals for Qualified Medical Expenses

Finally, when you withdraw money from your HSA to pay for qualified medical expenses, those withdrawals are also tax-free. This includes a wide range of expenses, from doctor visits and prescription medications to dental care and vision services. This tax-free withdrawal feature means you never pay taxes on the money you use for healthcare, completing the triple-tax advantage cycle.

This powerful combination of tax benefits makes HSAs an incredibly efficient tool for both managing current healthcare costs and building a robust financial future. By understanding and actively utilizing these advantages, individuals can significantly boost their overall financial health.

Maximizing Your HSA: Strategies for 12% Annual Growth

Achieving an annual growth rate of 12% with your Health Savings Account (HSA) in 2026 is an ambitious yet attainable goal, particularly for those who adopt smart investment strategies and understand the power of compounding. While past performance does not guarantee future results, a well-managed HSA investment portfolio can deliver substantial returns.

The key to maximizing growth lies in treating your HSA not just as a checking account for medical expenses but as a long-term investment vehicle. Many HSA providers offer a range of investment options, from conservative money market accounts to more aggressive stock and bond funds. Your investment choices should align with your risk tolerance and time horizon.

Strategic Investment Choices

To aim for higher growth, consider investing in diversified portfolios that include equity funds. Historically, the stock market has provided average annual returns that can support a 12% growth target over long periods. However, it’s essential to diversify to mitigate risk.

- Equity Funds: Invest in broad market index funds or ETFs for exposure to the stock market’s growth potential.

- Balanced Funds: For a more moderate approach, consider funds that balance stocks and bonds, adjusting the allocation as you near retirement.

- Long-Term Horizon: The longer your investment horizon, the more risk you can typically afford to take, increasing your potential for higher returns.

Another crucial strategy is to consistently contribute the maximum allowable amount each year. The more money you contribute and invest, the more capital you have working for you, benefiting from the tax-free growth. For 2026, keeping an eye on the IRS contribution limits is paramount to fully leverage your HSA’s potential.

Leveraging the Power of Compounding

Compounding is your greatest ally in achieving significant growth. When your investment earnings also start earning returns, the growth accelerates exponentially. By investing early and consistently, you give your HSA funds more time to compound, which is critical for reaching aggressive growth targets like 12% annually.

To truly maximize your HSA, prioritize paying for current medical expenses out-of-pocket if you can afford to, rather than drawing from your HSA. This allows your invested HSA funds to continue growing tax-free for as long as possible. You can even reimburse yourself later for past qualified medical expenses, provided you keep meticulous records.

HSA Contribution Limits and Changes for 2026

Understanding the annual contribution limits for Health Savings Accounts (HSAs) is crucial for maximizing their benefits. The IRS sets these limits annually, and for 2026, it’s important to be aware of any adjustments that may impact your savings strategy. These limits typically increase year over year to account for inflation and healthcare cost trends.

For individuals, there is a maximum amount you can contribute to your HSA each year. This limit applies to all contributions, whether made by you, your employer, or a third party on your behalf. Similarly, for families, a higher contribution limit is set to accommodate the broader healthcare needs of multiple individuals.

Individual and Family Contribution Limits

While the exact figures for 2026 are usually announced later in the year prior, historical trends suggest a continued increase. For context, in previous years, individual limits hovered around $4,000, and family limits around $8,000. It is vital to check the official IRS announcements for the precise 2026 figures as they become available.

- Individual Contribution Limit: The maximum amount an individual can contribute to their HSA.

- Family Contribution Limit: The maximum amount that can be contributed for those covered by a family HDHP.

Catch-Up Contributions for Those Over 55

For individuals aged 55 and older, the IRS allows for an additional “catch-up” contribution. This provision is designed to help older workers boost their healthcare savings as they approach retirement. This catch-up amount is also subject to annual adjustments and provides a significant opportunity for accelerated savings.

Staying informed about these limits ensures you can contribute the maximum allowable amount, taking full advantage of the tax deductions and the potential for tax-free growth. Regularly reviewing your contribution strategy in light of these changes is a best practice for HSA holders.

HSA vs. Other Retirement Accounts: A Comparative Advantage

When planning for retirement, individuals often weigh various savings vehicles. While 401(k)s and IRAs are well-known, the Health Savings Account (HSA) offers a distinctive comparative advantage, particularly for healthcare costs in retirement. Understanding these differences can help you make informed decisions about where to allocate your savings.

Unlike 401(k)s and traditional IRAs, which offer tax-deductible contributions and tax-deferred growth, HSAs provide the unique triple-tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. This makes the HSA an exceptionally powerful tool for healthcare savings, especially in retirement when medical costs tend to rise.

Key Differences and Synergies

While 401(k)s and IRAs are primarily designed for general retirement income, HSAs are specifically tailored for healthcare expenses. However, their flexibility allows them to function as a supplemental retirement account once you reach age 65.

- Tax Treatment: HSAs have the triple-tax advantage, while 401(k)s/IRAs typically offer tax-deferred growth (traditional) or tax-free withdrawals (Roth).

- Withdrawal Purpose: HSA withdrawals are tax-free for qualified medical expenses at any age. After age 65, HSA withdrawals for non-medical expenses are taxed as ordinary income, similar to traditional IRA withdrawals, but without the 10% early withdrawal penalty.

- Contribution Limits: Each account type has its own distinct contribution limits, which should be considered when planning your overall savings strategy.

For those who can afford to pay for current medical expenses out-of-pocket, an HSA can effectively become a stealth retirement account. By letting the funds grow untouched, you create a substantial nest egg specifically for future healthcare costs, which can be a significant financial burden in retirement.

Integrating an HSA into your broader financial plan can create powerful synergies. For example, maximizing your 401(k) or IRA contributions alongside your HSA can provide a well-rounded approach to retirement savings, addressing both general living expenses and anticipated healthcare needs.

Strategic Uses of HSA Funds Beyond Immediate Healthcare

While the primary purpose of a Health Savings Account (HSA) is to cover qualified medical expenses, its unique structure allows for strategic uses that extend far beyond immediate healthcare needs. Understanding these advanced strategies can significantly enhance your long-term financial planning and wealth accumulation.

One of the most powerful strategies is to treat your HSA as an investment vehicle for retirement. If you are in a position to pay for current medical expenses out-of-pocket, you can allow your HSA funds to grow tax-free over decades. This makes the HSA a highly effective, tax-advantaged savings account for future healthcare costs, or even general retirement expenses once you reach age 65.

Long-Term Investment and Reimbursement Strategy

By contributing the maximum to your HSA and investing those funds, you can build a substantial balance. Keep meticulous records of all qualified medical expenses you pay out-of-pocket. These expenses can be reimbursed from your HSA at any point in the future, tax-free. This means you could potentially let your HSA grow for 20, 30, or even 40 years, then withdraw a large sum tax-free to cover past medical expenses or future retirement healthcare costs.

- Record Keeping: Maintain detailed records of all medical receipts and Explanation of Benefits (EOB) forms.

- Delayed Reimbursement: Pay for current medical costs with other funds to allow your HSA to grow.

- Tax-Free Withdrawals: Reimburse yourself for past qualified medical expenses tax-free at a later date.

HSA as a Retirement Account After Age 65

Upon reaching age 65, your HSA essentially transforms into another retirement account, similar to a traditional IRA. While withdrawals for qualified medical expenses remain tax-free, you can also withdraw funds for non-medical expenses without incurring the 10% early withdrawal penalty. These non-medical withdrawals will be taxed as ordinary income, just like distributions from a traditional 401(k) or IRA.

This flexibility provides a safety net for retirement. If you have significant medical expenses, your HSA covers them tax-free. If your medical costs are lower than anticipated, you can use the funds for other retirement needs, albeit with income tax applied to non-medical withdrawals. This dual functionality makes the HSA an incredibly versatile and valuable asset in any long-term financial plan.

Navigating Future Healthcare Costs with Your HSA

The landscape of healthcare costs is constantly evolving, and planning for these future expenses is a critical component of financial stability. Your Health Savings Account (HSA) serves as an indispensable tool in navigating these uncertainties, providing a tax-advantaged way to save for both expected and unexpected medical expenditures in 2026 and beyond.

As individuals age, healthcare costs tend to increase significantly. Medicare, while comprehensive, does not cover all expenses, leaving gaps that an HSA can effectively fill. From deductibles and co-pays to prescription drugs and long-term care, having a robust HSA balance can alleviate much of the financial stress associated with healthcare in retirement.

Anticipating Retirement Healthcare Expenses

It’s a common misconception that Medicare covers all healthcare costs in retirement. In reality, retirees often face substantial out-of-pocket expenses. These can include Medicare premiums, deductibles, co-insurance, and services not covered by Medicare, such as dental, vision, and hearing care. An HSA is perfectly positioned to cover these costs tax-free.

- Medicare Premiums: Certain Medicare Part A, B, C, and D premiums can be paid with HSA funds.

- Long-Term Care Insurance: Premiums for qualified long-term care insurance can be paid from an HSA, up to certain age-based limits.

- Out-of-Pocket Costs: Deductibles, co-payments, and co-insurance for Medicare-covered services.

By consistently contributing to and investing your HSA throughout your working years, you build a substantial reserve specifically earmarked for these future expenses. This proactive approach can significantly reduce the financial burden of healthcare in retirement, allowing you to enjoy your golden years with greater peace of mind.

The Role of HSA in Financial Resilience

Beyond retirement, an HSA also contributes to overall financial resilience by providing a liquid, tax-advantaged fund for unexpected medical emergencies. Having these funds readily available means you can avoid dipping into other savings or incurring debt for health-related issues, safeguarding your financial progress.

In conclusion, leveraging your HSA effectively is about more than just current tax savings; it’s about building a powerful financial fortress against future healthcare costs, ensuring that health challenges don’t derail your financial well-being.

| Key Point | Brief Description |

|---|---|

| Triple-Tax Advantage | Contributions are tax-deductible, investments grow tax-free, and withdrawals for qualified medical expenses are tax-free. |

| Investment Potential | HSAs can be invested in various assets, allowing for significant long-term, tax-free growth, aiming for high annual returns. |

| Retirement Healthcare | HSAs are excellent for saving for future medical expenses in retirement, complementing Medicare coverage. |

| Contribution Limits | Annual IRS limits and catch-up contributions for those over 55 are crucial for maximizing benefits. |

Frequently Asked Questions About HSAs in 2026

To be eligible for an HSA in 2026, you must be covered by a High-Deductible Health Plan (HDHP), not have other health coverage (with few exceptions), not be enrolled in Medicare, and not be claimed as a dependent on someone else’s tax return. Specific HDHP minimums and maximums are set annually by the IRS.

The triple-tax advantage means contributions are tax-deductible, reducing your taxable income. Funds grow tax-free through investments, and withdrawals for qualified medical expenses are also tax-free. This combination makes HSAs highly efficient for both saving and spending on healthcare, with long-term growth potential.

Yes, an HSA can function as a powerful retirement account. After age 65, withdrawals for non-medical expenses are taxed as ordinary income, similar to a traditional IRA, but without the 10% early withdrawal penalty. Withdrawals for qualified medical expenses remain tax-free at any age, making it ideal for future healthcare costs.

HSA providers typically offer various investment options, ranging from conservative choices like money market accounts to more aggressive options such as mutual funds, exchange-traded funds (ETFs), and individual stocks. Diversification and aligning investments with your risk tolerance and time horizon are crucial for maximizing growth.

Your HSA is portable, meaning the funds belong to you, not your employer or health plan. If you change jobs or switch to a non-HDHP, you can no longer contribute to the HSA, but you retain ownership of the existing funds. You can continue to use them for qualified medical expenses or invest them for future use.

Conclusion

In summary, Health Savings Accounts (HSAs) in 2026 represent far more than just a savings vehicle for medical expenses; they are a cornerstone of effective financial planning, offering unparalleled tax advantages and significant wealth-building potential. By understanding the triple-tax benefits—tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses—individuals can strategically leverage HSAs to manage current healthcare costs while simultaneously building a robust financial foundation for retirement. The ability to invest these funds for long-term growth, potentially achieving annual returns of 12% or more, positions HSAs as a dynamic tool for securing both health and financial well-being. As healthcare costs continue to rise, proactive engagement with your HSA, adherence to contribution limits, and informed investment choices will be paramount to maximizing its benefits and ensuring a more secure future.